Save Money on a NT$35K Salary: 2026 Practical Guide for Young Workers in Taiwan

Prices keep climbing, salaries haven’t moved much — can you still save money on an NT$35,000 monthly income? Many people think it’s impossible, but in 2026 plenty of young coworkers around you are using a few simple strategies to stably save NT$8,000–12,000 each month. This article breaks down the four major expense buckets — rent, food, transportation, and savings — with the latest 2026 numbers (median rent, the TPASS NT$1,200 monthly pass, Richart 3.5% high-yield savings) all in one place.

1. Salary isn’t huge — what matters is spending where it counts

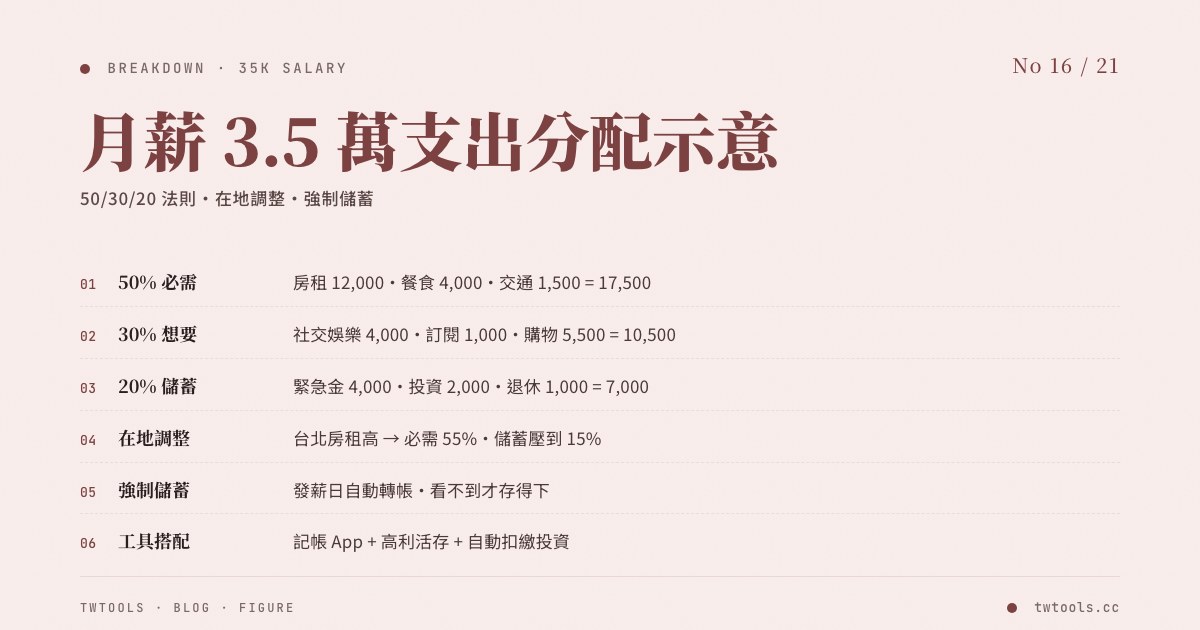

Taiwan’s CPI grew about 1.6% year over year in 2026 — gentler than the past two years, but for office workers on NT$30K–40K, every NT$1 still needs to count. Here’s a breakdown of how to allocate NT$35,000:

| Expense item | Typical range | Cost-saving version | Monthly savings |

|---|---|---|---|

| Rent (Taipei / New Taipei studio) | NT$15,000–20,000 | NT$6,000–10,000 (shared room) | NT$5,000–10,000 |

| Food | NT$8,000–10,000 | NT$4,000–6,000 (cooking 3–4 days a week) | NT$3,000–5,000 |

| Transportation | NT$2,500–4,000 (gas + parking) | NT$1,200 (TPASS monthly pass) | NT$1,500–2,500 |

| Phone + subscriptions | NT$1,500–2,500 | NT$800–1,200 | NT$500–1,000 |

| Miscellaneous + entertainment | NT$4,000–6,000 | NT$2,500–3,500 | NT$1,500–2,500 |

| Monthly savings | NT$0–2,000 | NT$8,000–12,000 | — |

The “cost-saving version” isn’t a vow of poverty — it’s choosing the right option for each expense, then auto-transferring the savings, so whatever’s left over can be spent however you like without going over budget. Item-by-item breakdown below.

Real-world example: Ms. A’s monthly NT$35,000 spending sheet

Ms. A, 27, shares a 3-bedroom flat in Zhonghe, New Taipei (NT$8,000 including utilities and management fees), cooks 3 days + eats out 4 days a week (NT$5,500 on food), uses the TPASS Greater Taipei NT$1,200 monthly pass, pays NT$1,000 for phone + two subscriptions, and spends about NT$3,000 on miscellaneous and entertainment. Monthly savings: NT$35,000 − NT$8,000 − NT$5,500 − NT$1,200 − NT$1,000 − NT$3,000 = NT$16,300. Of that, NT$10,000 auto-transfers into Richart at 3.5%, NT$5,000 goes into a fixed monthly 0050 purchase, and NT$1,300 stays as flexible buffer. Principal + interest after one year comes to about NT$130,000–140,000; after 5 years, with ETF compounding, total assets approach NT$800,000.

2. Rent: 2026 Taipei / New Taipei — shared room vs studio vs living with family

Rent is the biggest expense — saving on rent alone offsets a full round of cuts on everything else. Latest 2026 market rates:

- Shared room in Taipei / New Taipei: NT$6,000–10,000 (cheaper on the outer ends of the MRT — Xinzhuang, Shulin, Yonghe, etc.; pricier in East District Taipei, Xinyi, and Banqiao business areas)

- Studio apartment: NT$15,000–25,000 (elevator building including management fees; New Taipei prime areas have crossed NT$1,000 per ping in monthly rent starting 2025)

- Living at home, contributing monthly: NT$3,000–5,000 (the cheapest option, depending on family situation)

Shared rooms save money — but watch 3 things

- Sub-leasing risk: confirm landlord identity before signing — ask to see a property tax bill or title deed

- Lease legality: only properties properly registered for “residential use” qualify for the rent deduction

- Deposit capped at 2 months: under the Rental Housing Market Development and Management Regulations, charging more than 2 months is illegal

Don’t forget to claim the rent deduction

Starting 2026, the rent deduction is raised to a special deduction of NT$180,000/year (retroactively effective from tax year 2025). Monthly rent of NT$8,000 × 12 = NT$96,000; for income under NT$500,000/year (5% bracket), that’s about NT$4,800 back in your pocket. See the 2026 tax filing complete guide for details.

3. Food: the real gap between cooking and eating out

Eating out for lunch and dinner at NT$300/day adds up to about NT$9,000 a month. Cook for yourself 3–4 days a week and the groceries + gas come to about NT$3,000–4,000 a month — that alone saves NT$4,000–5,000.

Real cooking cost in 2026 (one month)

- Vegetables (from a traditional market): NT$800–1,200 (20–30% cheaper than supermarkets)

- Meat / eggs (about 2 kg of chicken breast + 30 eggs per week): NT$1,200–1,500

- Seasonings / rice / noodles: NT$500–700

- Extra utilities from cooking at home: NT$300–500

- Total: NT$2,800–3,900/month (26–30 lunch and dinner meals)

Eating out, but on a budget

For days you can’t cook, the “bento strategy” helps: get a NT$90–110 cafeteria-style lunch, cook something simple at home for dinner — average about NT$200/day, NT$6,000/month total.

Drinks add up faster than you think

A bubble tea at NT$50–70 three times a week comes to NT$800–900 a month. Switching to your own coffee or tea bags saves over NT$10,000 a year.

4. Transportation: TPASS NT$1,200 monthly pass vs scooter

A lot of people assume the TPASS NT$1,200 pass must have a catch — it doesn’t. It’s a 2023 central + local government subsidy that’s been operating steadily since 2024, with TPASS 2.0 frequent-rider rewards launching on 2026-01-14.

Monthly pass prices by region

- Greater Taipei (Taipei, New Taipei, Keelung, Taoyuan): NT$1,200 (covers MRT, buses, TRA regional trains, some intercity buses, and YouBike free for the first 30 minutes)

- Central Taiwan (Taichung, Changhua, Nantou, Miaoli): NT$699 or NT$999

- Southern Taiwan (Tainan, Kaohsiung, Pingtung): NT$999

- Single-city pass: Tainan / Kaohsiung / Pingtung intra-city at NT$399

TPASS 2.0 frequent-rider rewards (from 2026)

After registering your e-ticket with the Highway Bureau’s frequent-rider reward area, taking 11+ rides in a month qualifies you for rewards, with the reward rate tiered by ride count. Effectively the pass price drops another notch.

Scooter vs monthly pass — the math

| Item | Scooter | TPASS monthly pass |

|---|---|---|

| Gas | NT$1,200–1,800 | NT$0 |

| Parking | NT$600–1,500 | NT$0 |

| Insurance / license tax / maintenance amortization | NT$500–800 | NT$0 |

| Monthly pass | NT$0 | NT$1,200 |

| Total | NT$2,300–4,100 | NT$1,200 |

As long as your daily commute is under 20 km and stays inside a major metropolitan area, TPASS beats a scooter. The remaining distance / occasional trips outside the city can be handled with YouBike + intercity buses.

5. Savings and investing: high-yield savings + monthly ETF auto-buys

Handle saved money in two layers: build the emergency fund first → then start regular monthly investing.

Emergency fund: 3–6 months of living expenses, parked in a high-yield account

2026 digital account high-yield savings rates (Q2 published):

| Bank | New-account rate | Cap | Existing-account / notes |

|---|---|---|---|

| Taishin Richart | 3.5% | First NT$300K (2026-03-02 to 2026-07-01) | Existing accounts: 1.8% on first NT$300K |

| NEXT Bank | 2% | First NT$200K + 1.5% above NT$50K with no cap | Same rate for new and existing accounts |

| SinoPac DAWHO | 1.5% | First NT$300K | Through 2026-06-30 |

| Union Bank NewNewBank | Up to 15% | Lower balance cap | New accounts only |

Strategy: first save up 3 months of living expenses (about NT$100,000–150,000) in Richart or NEXT Bank for the interest. Once that’s funded, consider other uses.

Monthly ETF auto-buy: the long-term power of compounding

Buy NT$3,000–5,000 of 0050 (Yuanta Taiwan 50) or a high-dividend ETF (0056, 00919) on a fixed monthly schedule. 0050’s annualized total return (including dividends) over the past 5 years has been around 10.88% — far ahead of a savings account. NT$5,000/month for 10 years (compounding at an 8% assumption) accumulates to about NT$920,000.

Auto-transfer: the iron rule of “save first, spend what’s left”

Open your bank app, set up an automatic transfer from your salary account → savings account, and route NT$8,000–10,000 to Richart or NEXT Bank the day after each payday. Money you don’t see is money you don’t spend. This works at least 3× more reliably than “let’s see what’s left at month-end.”

6. FAQ

Q1: I’m already 30 and still on NT$35K — should I switch jobs?

A: Saving and switching jobs aren’t either-or. A NT$35K salary still leaves room to grow. Do both: ① use this article’s strategies to save NT$10K/month and build a financial cushion, ② learn new skills or earn certifications to gradually push salary up. The bigger the cushion, the more aggressively you can target higher-paying roles when you do switch.

Q2: Does sharing a flat really save that much? Aren’t roommates a hassle?

A: Shared housing can save NT$5,000–10,000, but factor in the social cost. Aim for 2–3-bedroom layouts where each tenant has their own work/sleep schedule (avoid roommates who are unemployed and home all day), use written agreements for splitting utilities and shared supplies, and clarify everything up front.

Q3: Will the high-yield savings rates stay this high?

A: No. Richart’s 3.5% runs from 2026-03-02 to 2026-07-01; most banks’ high-yield offers are short-term promotions and may drop back to 1.5–2% afterward. Keep an eye on bank announcements, or just re-evaluate accounts every 6 months.

Q4: 0050 has already risen a lot — is it too late to start?

A: The core of regular monthly buying is spreading time risk. The “highest point vs lowest point” question matters less for long-term investors. 0050’s underlying basket is Taiwan’s top 50 stocks by market cap, and it tracks the Taiwan economy’s overall growth — on a 5–10 year horizon, it tends to keep pace with the market. What matters isn’t “when to start” — it’s “keep going.”

Q5: 0050 vs 0056 vs 00919 — which to pick?

A: 0050 is a market-cap-weighted index pursuing capital gains — about 10.88% annualized total return over the past 5 years, with a 1.39–2% dividend yield. 0056 and 00919 are high-dividend ETFs prioritizing payouts — 5–7% yields but weaker capital appreciation. Young people accumulating principal are usually best off mainly in 0050, with 10–20% in 0056 / 00919 for dividend income. Closer to retirement, gradually shift more toward the high-dividend side.

Q6: Should I use credit cards? Won’t I accidentally max them out?

A: Credit cards themselves aren’t the problem — “swiping without reconciling” is. Recommendations: ① only get 1–2 cards with practical rewards (a household-bills card + an overseas card), ② reconcile every statement, annotating any unexpected charges, ③ set automatic full-balance payment to avoid revolving interest (7–15% APR), ④ track monthly credit spending as a share of your salary — if it crosses 30%, time to course-correct.

7. Re-examining your budget in a 2026 inflationary environment

In past years, you could slowly save up by tight budgeting alone with no investing. The 2026 environment is different — you have to actively rebalance your budget against the inflation numbers.

2026 inflation numbers: mild but persistent

DGBAS data: CPI inflation was 1.75% in February 2026, slowing to 1.2% in March. Not the 3%+ peak of 2022–2023, but it still keeps chipping away at purchasing power. For an NT$35,000 office worker, inflation alone reduces real purchasing power by roughly NT$5,000–8,000 per year — so “salary stays flat” = “you’re moving backward.”

Where NT$35K sits relative to the 2026 minimum wage

Starting January 2026, the minimum wage rises to NT$29,500/month or NT$196/hour. NT$35,000 sits about 18% above minimum wage — the “slightly above the bottom” tier. If your salary hasn’t grown in 5 years, your real purchasing power is actually below what NT$35K bought in 2020. That’s not alarmist — it’s just the math.

Three common budget allocation rules (NT$35K calculated out)

| Rule | Savings | Living | Other | Best for |

|---|---|---|---|---|

| 3-3-3 rule | NT$11,667 | NT$11,667 (living) | NT$11,667 (emergency fund) | Beginners just learning to save |

| 6-3-1 rule | NT$10,500 | NT$21,000 (living) | NT$3,500 (insurance) | High-rent / high-commute Taipei / New Taipei dwellers |

| 4-3-2-1 rule | NT$7,000 | NT$10,500 (living) | NT$14,000 (investing) + NT$3,500 (insurance) | Advanced planners who already have an emergency fund |

Recommended allocation for NT$35K:

- Savings + investing: NT$10,000–12,000 (high-yield savings + monthly ETF buys)

- Living essentials (rent / food / transit): NT$18,000–20,000

- Personal enjoyment + learning: NT$3,000–5,000

- Insurance + emergency buffer: NT$2,000–3,000

The key is automated routing — on payday, the system moves the savings portion before you see it, and what’s left is for living. Saving first then spending is a wealth mindset; spending first then saving leaves you in debt.

A minimum-viable list for fighting inflation: prioritize these 3

- Open a NT$1,000–3,000/month new income stream: pick up 1–2 light side hustles (design, copywriting, admin help) — the growth dwarfs 1–2% inflation (further reading: side hustle tools and tax guide)

- Switch to dividend-bearing ETFs: 0050’s 10.88% annualized total return easily beats 1.2% inflation — let the assets outrun prices on their own

- Avoid “fake discounts”: “promotional prices” at big-box and online retailers often already bake in a price hike; compare current unit prices against historical ratios to see the real picture

Inflation isn’t the end of the world, but ignoring it slowly erodes your effort. Spend 5 minutes tonight listing your subscriptions and assess which one or two to cut — fastest concrete way to demonstrate “I’m actively responding to inflation.”

Conclusion

Saving on an NT$35K salary isn’t about extreme frugality — it’s about picking the right option + automating. Shared room or living with family saves NT$5,000–10,000; TPASS replaces a scooter for NT$2,000–3,000 saved; cooking 3–4 days a week saves NT$4,000–5,000; auto-transferring salary into Richart earns the 3.5% — the gap of NT$8,000–12,000 per month is right there.

What you save goes into a 3–6 month emergency fund (high-yield savings) plus NT$3,000–5,000/month into ETFs. After 10 years, compounding alone gets you near NT$1M. Money doesn’t multiply on its own, but it does earn interest on its own. One thing to do today: open your bank app and set up the auto-transfer — starting next month, things will look different. 5 minutes of monthly decision cost opens up 10 years of future optionality.

Further reading: Emergency fund complete guide: how much to save and where to keep it, Emergency fund calculator, 2026 tax filing complete guide.