2026 Tax Filing: Education, Tuition, and Tutoring Deductions Plus New Brackets to Save NT$20,000

In May tax season, you may have left education deductions on the table

Plenty of office workers spend tens of thousands of NT dollars a year on their kids’ education (tuition, tutoring, talent classes, and more), but they don’t know how much of it qualifies as a deduction at tax time. Some deductions the government never proactively flags — you only cut your tax bill if you claim them yourself. The 2026 filing season (reporting tax year 2025 income) introduces several new rules, so if you have children’s education expenses, read this carefully.

2026 filing basics — start here

Tax season runs May 1 to May 31, 2026. Major changes this year (reporting tax year 2025 income):

| Item | Tax Year 2024 (2025 filing) | Tax Year 2025 (2026 filing) | Change |

|---|---|---|---|

| General personal exemption | NT$92,000 | NT$97,000 | +NT$5,000 |

| Personal exemption (age 70+) | NT$138,000 | NT$145,500 | +NT$7,500 |

| Standard deduction (single) | NT$124,000 | NT$131,000 | +NT$7,000 |

| Standard deduction (married joint) | NT$248,000 | NT$262,000 | +NT$14,000 |

| Special deduction for salaries | NT$218,000 | NT$227,000 | +NT$9,000 |

| Special deduction for long-term care | NT$120,000 | NT$180,000 | +NT$60,000 (50% jump) |

| Preschool (1st child) | NT$150,000 | NT$150,000 | Unchanged |

| Preschool (2nd child and beyond) | NT$225,000 | NT$225,000 | Unchanged |

| Basic living allowance (per person) | NT$202,000 | NT$213,000 | +NT$11,000 |

Two items that matter most to middle-class families: the long-term care special deduction jumps from NT$120,000 to NT$180,000 (saves NT$7,200 for someone earning over NT$80,000 monthly in the 12% bracket), and the basic living allowance hits NT$213,000 — which shifts the “minimum standard of living” threshold.

2026 individual income tax brackets and rates

| Net Comprehensive Income | Tax Rate |

|---|---|

| NT$0 – 590,000 | 5% |

| NT$590,000 – 1,330,000 | 12% |

| NT$1,330,000 – 2,660,000 | 20% |

| NT$2,660,000 – 4,980,000 | 30% |

| Over NT$4,980,000 | 40% |

Knowing your bracket lets you calculate how much each extra NT$10,000 of deductions saves. For example, in the 12% bracket every NT$10,000 of deductions saves NT$1,200; in the 20% bracket, NT$2,000.

Education-related deductions

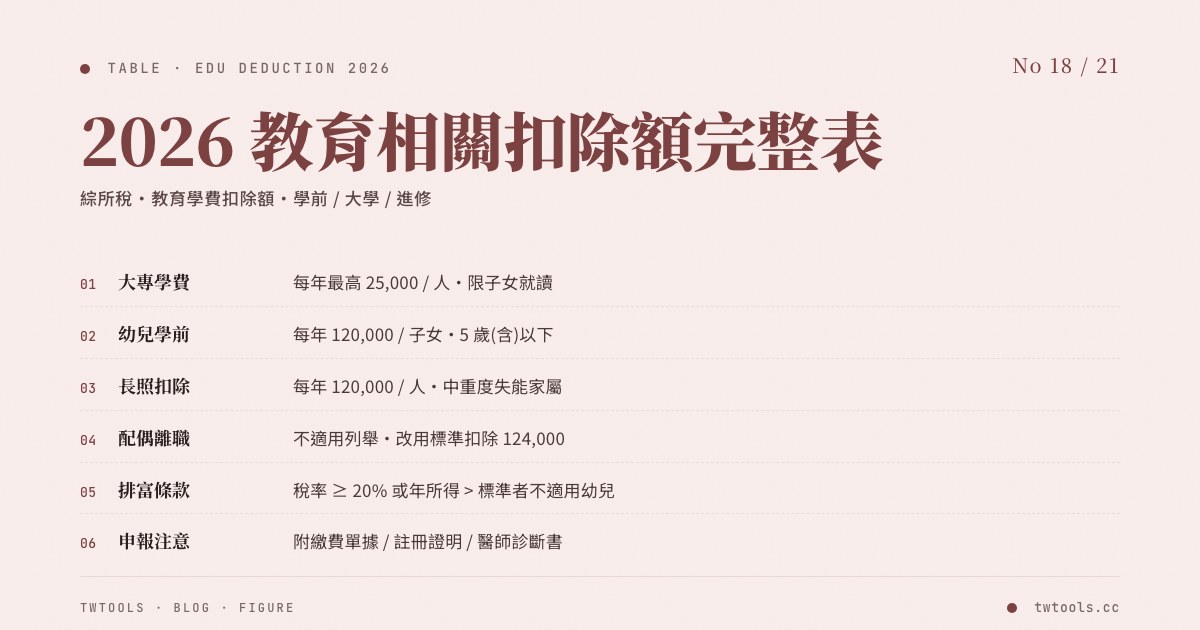

1. Special deduction for children’s tuition (most common)

If you support a child enrolled at a junior college or above recognized in Taiwan, you can deduct NT$25,000 of tuition per child per year (tuition must have been paid within the tax year or paid in installments).

- Eligibility: Children enrolled at MOE-recognized junior colleges and above (universities, technical colleges, 4-year technical institutes), domestic or overseas.

- Amount: Cap of NT$25,000 per child per year.

- Multiple children: Three kids in college → deduct NT$25,000 each, NT$75,000 total.

- Not eligible: Open University, Open Junior College, the first 3 years of 5-year junior colleges (years 1–3), language schools.

- Common gaps: Dorm fees and book fees typically aren’t deductible — only “tuition + miscellaneous fees.” Check whether your payment receipt reads “tuition” or “accommodation.”

2. Special Preschool Deduction (substantially raised in 2026)

The tax year 2025 rules raised the deduction significantly and removed the wealth-exclusion clause (previously, taxpayers in the 20% bracket and above couldn’t use it; now all brackets qualify):

- 1st child: NT$150,000 per year (raised from NT$120,000).

- 2nd child and beyond: NT$225,000 per year (unchanged at NT$225,000).

- Eligibility: Children under age 6 (raised from under age 5).

- Applies to: Children enrolled in licensed kindergartens, daycare centers, or registered nanny care.

⚠️ Common confusion: Many old articles cite “NT$12,000 + children under age 5” — that’s the 2024 rules and no longer applies to 2026 filing. If you see a guide quoting NT$12,000 for 2026, skip it.

3. Children’s education expenses (private junior high and below)

Tuition for private junior high school or private senior high school (vocational schools excluded) gets you a small additional deduction when claiming the child as a dependent. The mechanism isn’t a “direct deduction” — instead, you flag it when listing dependents and the tax authority calculates the savings.

- No deduction for public schools: Government-subsidized public middle and high schools don’t get an extra deduction.

- Civil servants’ education subsidy for children: If you’re a civil servant, this amount is subsidized directly by the government, so you don’t claim it again at tax time.

4. Tutoring and talent classes? Usually no — but there are exceptions

General tutoring schools and music, art, or sports talent classes typically can’t be deducted on the individual income tax return. Two exceptions:

- Long-term care “home-care course fees”: If you take a government-approved care-training course (the long-term care special deduction rises to NT$180,000 in 2026), the fee qualifies.

- Lifelong learning courses (subsidized in some regions): A few counties offer “active senior learning” or “senior continuing education” subsidies, but those are direct subsidies, not tax deductions.

Worked examples for dual-income families (2026 rules)

Example A: Dual-income, Spouse A supports two parents, Spouse B supports 2 children

Spouse A (NT$60,000 monthly, NT$720,000 annual):

- General personal exemption: NT$97,000 (self)

- Supporting father: NT$97,000

- Supporting 80-year-old mother: NT$145,500

- Standard deduction (couple): NT$262,000 (shared by both spouses)

- Special salary deduction: NT$227,000

Spouse B (NT$50,000 monthly, NT$600,000 annual):

- General personal exemption: NT$97,000

- Supporting Child A (college student): NT$97,000 + tuition NT$25,000

- Supporting Child B (age 4): NT$97,000 + Preschool Deduction NT$150,000 (1st child)

- Special salary deduction: NT$227,000

Total household deductions: 9.7×4 + 14.55 + 26.2 + 22.7×2 + 2.5 + 15 = NT$1,484,500

Total household annual income NT$1,320,000 − total deductions NT$1,484,500 = negative, no tax owed (basic living allowance NT$213,000 × 4 = NT$852,000 is already covered).

Example B: Single-income family, 2 children at different education levels

Primary earner (NT$80,000 monthly, NT$960,000 annual):

- General personal exemption: NT$97,000 (self)

- Supporting spouse: NT$97,000

- Supporting Child A (college student): NT$97,000 + tuition NT$25,000

- Supporting Child B (age 5): NT$97,000 + Preschool Deduction NT$150,000 (1st child)

- Standard deduction (couple): NT$262,000

- Special salary deduction: NT$227,000

Total deductions: 9.7×4 + 26.2 + 22.7 + 2.5 + 15 = NT$1,052,000

Net taxable amount: 96 − 105.2 = −NT$92,000 (tax owed: 0).

Adding the NT$180,000 long-term care special deduction (if the spouse is caring for an elder) drops the tax base even further — the new NT$180,000 long-term care provision really pays off here.

How much tax can you actually save in a year?

Suppose you earn NT$60,000 a month (NT$720,000 a year), supporting 1 college student and 1 toddler (age 5). Without claiming these deductions, you’d land in the 12% bracket:

| Deduction | Amount | Tax Saved at 12% |

|---|---|---|

| Child’s tuition | NT$25,000 | NT$3,000 |

| Preschool (1st child) | NT$150,000 | NT$18,000 |

| Long-term care special deduction (spouse caring for elder) | NT$180,000 | NT$21,600 |

| Total annual savings | NT$355,000 | NT$42,600 |

For a family earning NT$60,000 a month, claiming the right education and long-term care deductions saves over NT$40,000 a year — roughly an extra month of disposable income.

How to make sure you don’t miss these deductions

1. Prepare complete proof of payment

- University: Tuition invoice, payment receipt (attach to the tax return when submitted for audit).

- Kindergarten / nanny: Monthly payment receipts or annual invoices (keep originals or copies through the May filing).

- Long-term care course: Course receipt + the host organization’s registration certificate.

2. Check the right boxes when filing online

In the MOF’s e-filing system, go to “Basic Information” → “Dependents” and verify each child’s fields:

- Check “tuition” + amount (university).

- Check “preschool” + amount (under age 6).

- Check “long-term care” (if there’s someone needing care).

3. Pick one of the multi-factor authentication methods

The 2026 e-filing system has 6 login methods: mobile-phone authentication / NHI card + registration password / Citizen Digital Certificate / Mobile Citizen Digital Certificate / household registration number + lookup code / Financial Certificate. Mobile-phone authentication is the easiest — login in about 1 minute.

4. Visit the tax office in person

If you’re uneasy about the online system, bring all your receipts and ID to the local tax office and file at the counter. Staff will help you check whether you’ve missed any deductions.

5. Watch the timing

Some deductions require the expense to be “paid within the tax year” — for example, tuition must be paid between January and December 2025 to qualify for the May 2026 filing. Prepaid or deferred fees may fall in different tax years.

FAQ

Q1: How does the “NT$225,000 from the 2nd child onward” preschool deduction work? A: Every 2nd, 3rd, and subsequent child (under age 6) in the family deducts NT$225,000. 1st child NT$150,000 + 2nd child NT$225,000 + 3rd child NT$225,000 = NT$600,000. Families with 3 young children see major tax savings.

Q2: My child is a college freshman who enrolled in September 2025. Can the tuition be deducted in the May 2026 filing? A: Yes. Tuition paid in the second half of 2025 falls under “tax year 2025” and gets claimed in the May 2026 filing. But the next-semester tuition you’ll pay in February 2026 belongs to “tax year 2026” and can only be deducted in the May 2027 filing.

Q3: How do I sequence deductions for maximum savings? A: Pick standard or itemized — you can’t use both. For most families, the standard deduction (NT$262,000 for a couple) is the easier path, unless your large medical bills, donations, and home mortgage interest exceed NT$262,000. Special deductions (education, preschool, long-term care) stack on top of either standard or itemized.

Q4: Single and childless — what should I watch for in 2026 filing? A: ① The standard deduction rises to NT$131,000, ② the special salary deduction rises to NT$227,000, ③ the basic living allowance is NT$213,000 — the combined tax-exempt threshold goes up by about NT$23,000. Workers earning under NT$40,000 a month basically owe no tax.

Filing in May isn’t just an “obligation” — it’s an annual chance to cut your tax bill legally. Families with kids in school plus elderly relatives who need care should especially comb through every available deduction. Before the May 31 deadline, gather every supporting document so nothing slips through.